STATE OF IOWA

[STATE TAX TRIBUNAL / DEPARTMENT OF REVENUE]

In re the Matter of the Appeal of

[TAXPAYER NAME], Petitioner

PETITION FOR APPEAL OF TAX ASSESSMENT

(and Request for Collection Stay)

Effective Date: [DATE OF FILING]

Governing Law: Iowa state tax law, the Iowa Administrative Procedure Act (Iowa Code ch. 17A), and all applicable administrative rules

Forum Selection: State Tax Tribunal / Director of Revenue (as applicable)

[// GUIDANCE: Replace bracketed language with client-specific information. Optional provisions appear in shaded italics. Delete any that do not apply.]

TABLE OF CONTENTS

- Document Header ........................................................................................... 1

- Definitions ......................................................................................................... 2

- Jurisdiction and Venue .................................................................................... 3

- Procedural History ............................................................................................ 3

- Grounds for Appeal ........................................................................................... 4

- Relief Requested ............................................................................................... 5

- Representations & Warranties .......................................................................... 6

- Covenants & Ongoing Obligations ................................................................... 7

- Burden of Proof & Evidentiary Standards ...................................................... 8

- Collection Stay ................................................................................................ 8

- Default & Remedies ....................................................................................... 9

- Risk Allocation ............................................................................................... 10

- Dispute Resolution ....................................................................................... 11

- General Provisions ....................................................................................... 12

- Verification ..................................................................................................... 13

- Certificate of Service ..................................................................................... 14

- Execution Block ............................................................................................. 15

(Page numbers auto-update in word-processing software.)

1. DOCUMENT HEADER

1.1 Parties

(a) Petitioner: [TAXPAYER NAME], a [ENTITY TYPE] organized under the laws of [STATE] with its principal place of business at [ADDRESS].

(b) Respondent: Iowa Department of Revenue (the “Department”), acting through its Director or such other officer as may be designated by law.

1.2 Recitals

A. On [DATE OF ASSESSMENT] the Department issued to Petitioner a Notice of Assessment and Demand for Payment in the amount of $[AMOUNT] (the “Assessment”).

B. Petitioner timely files this Petition pursuant to Iowa Code ch. 17A and applicable Department rules within the statutory appeal period.

C. Petitioner seeks review, modification, or abatement of the Assessment and requests a stay of collection activity during the pendency of this appeal.

2. DEFINITIONS

The following capitalized terms have the meanings set forth below. Terms defined in the singular include the plural and vice-versa. Cross-references are to Sections of this Petition unless otherwise noted.

“Administrative Proceeding” means the contested-case process governed by Iowa Code ch. 17A and Department rules.

“Assessment” has the meaning given in Recital A.

“Collection Stay” means the suspension of enforcement or collection actions relating to the Assessment during the pendency of this appeal, as allowed by law.

“Department” has the meaning given in Section 1.1(b).

“Director” means the Director of Revenue for the State of Iowa or the Director’s authorized designee.

“Petitioner” has the meaning given in Section 1.1(a).

“Petition” means this Petition for Appeal of Tax Assessment, together with all exhibits, schedules, and supplements.

“State Tax Tribunal” means the forum selected for adjudication of this Petition, whether the independent Iowa Tax Tribunal or an ALJ assigned by the Department (collectively, the “Tribunal”).

3. JURISDICTION AND VENUE

3.1 This Tribunal has subject-matter jurisdiction under Iowa Code ch. 17A and other applicable provisions of Iowa tax law.

3.2 Venue is proper because the Assessment was issued by the Department and Petitioner has elected the administrative appeal forum authorized by statute.

4. PROCEDURAL HISTORY

4.1 Assessment Issuance. [Briefly summarize notice number, date mailed, tax type, taxable periods, and statutory authority cited by the Department.]

4.2 Timeliness of Appeal. Petitioner received the Assessment on [DATE] and submits this Petition within [##] days, thereby satisfying the statutory filing deadline.

4.3 Exhaustion of Administrative Remedies. Petitioner has (or has not) requested an informal conference per Department rules. [If an informal conference occurred, describe outcome; if waived, state so.]

5. GROUNDS FOR APPEAL

Petitioner contests the Assessment on the following independent and cumulative grounds:

5.1 Factual Error. The Department erroneously included or omitted [SPECIFIC ITEM], resulting in an overassessment of $[AMOUNT].

5.2 Legal Error. The Department misapplied Iowa Code § [SECTION] by treating [ISSUE] as taxable.

5.3 Procedural Defect. The Assessment is void/voidable because the Department failed to provide required notice under Iowa Code § [SECTION] and corresponding rules.

5.4 Constitutional Grounds. [Optional] The Assessment violates the Due Process Clause of the Iowa Constitution because [EXPLAIN].

5.5 Alternative Positions. Without conceding liability, Petitioner asserts alternative computations showing the maximum correct tax of $[AMOUNT].

[// GUIDANCE: List each disputed adjustment separately. Attach schedules and supporting exhibits.]

6. RELIEF REQUESTED

Petitioner respectfully requests that the Tribunal:

6.1 Modify or abate the Assessment to the extent of $[AMOUNT] (or in full).

6.2 Declare that no additional tax, penalty, or interest is due for the periods at issue.

6.3 Grant a Collection Stay under Section 10 pending final, non-appealable resolution of this matter.

6.4 Award statutory costs, reasonable attorneys’ fees where permitted, and such other relief as equity requires.

7. REPRESENTATIONS & WARRANTIES

Petitioner represents and warrants to the Tribunal and the Department that:

7.1 Organization and Authority. Petitioner is duly organized, validly existing, and in good standing under the laws of its jurisdiction of formation, with authority to prosecute this appeal.

7.2 Accuracy of Information. All factual statements, schedules, and exhibits submitted with this Petition are, to the best of Petitioner’s knowledge and belief, true, correct, and complete.

7.3 Compliance with Law. Petitioner has complied in all material respects with applicable filing deadlines, payment requirements, and administrative rules prerequisite to this appeal.

7.4 No Fraudulent Purpose. This Petition is not interposed for delay and is filed in good faith.

7.5 Survival. The foregoing representations survive dismissal, withdrawal, or final resolution of this Petition.

8. COVENANTS & ONGOING OBLIGATIONS

8.1 Cooperation. Petitioner shall cooperate with reasonable Department discovery requests, including production of documents and witness availability, subject to applicable privileges.

8.2 Supplemental Filings. Petitioner will promptly supplement or correct any material misstatement or omission identified after filing this Petition.

8.3 Payment of Undisputed Amounts. Petitioner shall remit all portions of the Assessment not contested herein, unless otherwise stayed by law or order.

8.4 Notice of Change. Petitioner shall notify the Tribunal and the Department within ten (10) days of any change in contact information or legal representation.

9. BURDEN OF PROOF & EVIDENTIARY STANDARDS

9.1 Pursuant to Iowa law, the taxpayer bears the burden of proving by a preponderance of the evidence that the Assessment is erroneous.

9.2 Evidentiary submissions shall comply with Tribunal rules regarding format, authentication, and deadlines.

[// GUIDANCE: Attach an evidentiary index to streamline admission of exhibits.]

10. COLLECTION STAY

10.1 Automatic Stay. Upon timely filing of this Petition and compliance with any bonding or security requirements set by the Department, collection activity on the disputed Assessment shall be stayed as provided by law.

10.2 Scope of Stay. The stay prohibits levy, garnishment, or other enforced collection but does not toll statutory interest unless expressly ordered.

10.3 Termination. The stay terminates upon (i) final, non-appealable adjudication of this matter, (ii) Petitioner’s written withdrawal of the Petition, or (iii) failure to comply with Tribunal orders.

11. DEFAULT & REMEDIES

11.1 Events of Default. The following constitute a default by Petitioner:

(a) Failure to prosecute the appeal;

(b) Failure to comply with discovery or scheduling orders;

(c) Non-payment of undisputed tax liabilities;

(d) Material misrepresentation to the Tribunal.

11.2 Department Remedies. Upon default, the Tribunal may dismiss this Petition with prejudice, lift the Collection Stay, and reinstate the Assessment in full.

11.3 Cure Period. Petitioner shall have ten (10) business days after written notice of default to cure, unless the Tribunal orders otherwise.

12. RISK ALLOCATION

12.1 Indemnification (Taxpayer Burden of Proof). Petitioner acknowledges and agrees that, as the party challenging the Assessment, it bears all risks associated with failure to meet its burden of proof.

12.2 Limitation of Liability. The Department’s monetary exposure is strictly limited to adjustment or refund of the Assessment, plus any statutory interest. Neither party is liable for incidental, consequential, or punitive damages.

12.3 Force Majeure. Deadlines may be extended for force-majeure events (e.g., natural disaster, declared emergency) upon motion and good-cause showing.

13. DISPUTE RESOLUTION

13.1 Governing Law. This Petition and all related proceedings are governed by Iowa law.

13.2 Forum Selection. Exclusive jurisdiction lies with the State Tax Tribunal / Director of Revenue, subject to judicial review in state district court under Iowa Code ch. 17A.

13.3 Limited Arbitration. If mutually agreed in writing, discrete factual disputes (e.g., sampling methodology) may be submitted to binding arbitration under the Iowa Uniform Arbitration Act, provided the Tribunal retains jurisdiction over all legal determinations.

13.4 Jury Waiver. To the extent a jury trial might otherwise be available upon judicial review, the parties knowingly waive that right except as constitutionally mandated.

13.5 Injunctive Relief. Nothing in this Section limits either party’s right to seek emergency injunctive relief to enforce or modify the Collection Stay.

14. GENERAL PROVISIONS

14.1 Amendment. This Petition may be amended once as a matter of right within the time allowed by Tribunal rule; further amendments require leave of the Tribunal.

14.2 Assignment. Petitioner may not assign rights or delegate obligations arising from this Petition without prior Tribunal approval.

14.3 Severability. If any provision is held unlawful or unenforceable, the remaining provisions remain in full force, and the Tribunal may reform the Petition to preserve its original intent.

14.4 Integration. This Petition, including all exhibits and schedules, constitutes the entire statement of claims and defenses regarding the Assessment.

14.5 Electronic Signatures. Signatures executed and transmitted electronically (e.g., via PDF) are deemed original for all purposes.

15. VERIFICATION

I, [AUTHORIZED REPRESENTATIVE NAME], being first duly sworn, state that I am [TITLE] of [TAXPAYER NAME] and that I have read the foregoing Petition. To the best of my knowledge and belief, the statements contained herein are true, correct, and complete.

text

_____________________________________

[AUTHORIZED SIGNATORY]

Subscribed and sworn before me this ___ day of __________, 20__.

text

_____________________________________

[NOTARY PUBLIC]

My Commission Expires: __________

16. CERTIFICATE OF SERVICE

I certify that on this ___ day of __________, 20__, a true and correct copy of the foregoing Petition (including all exhibits) was served upon the Iowa Department of Revenue, Legal Services and Appeals Division, by:

☐ First-class U.S. Mail ☐ Hand Delivery ☐ Certified Mail ☐ Electronic Mail (if authorized)

text

_____________________________________

[NAME], Counsel for Petitioner

17. EXECUTION BLOCK

Executed on the Effective Date by the duly authorized representatives of the parties.

For Petitioner:

text

_____________________________________

[NAME]

[TITLE]

[TAXPAYER NAME]

Date: __________

For Respondent (Acknowledgment of Receipt Only):

text

_____________________________________

[NAME]

[Title], Iowa Department of Revenue

Date: __________

Acknowledgment does not constitute consent to the relief requested.

[// GUIDANCE: Before filing, confirm current filing fee, bonding requirements, and method of delivery accepted by the Tribunal. Attach all supporting schedules, calculations, and documentary evidence in sequentially numbered exhibits.]

Do more with Ezel

This free template is just the beginning. See how Ezel helps legal teams draft, research, and collaborate faster.

AI that drafts while you watch

Tell the AI what you need and watch your document transform in real-time. No more copy-pasting between tools or manually formatting changes.

- Natural language commands: "Add a force majeure clause"

- Context-aware suggestions based on document type

- Real-time streaming shows edits as they happen

- Milestone tracking and version comparison

Research and draft in one conversation

Ask questions, attach documents, and get answers grounded in case law. Link chats to matters so the AI remembers your context.

- Pull statutes, case law, and secondary sources

- Attach and analyze contracts mid-conversation

- Link chats to matters for automatic context

- Your data never trains AI models

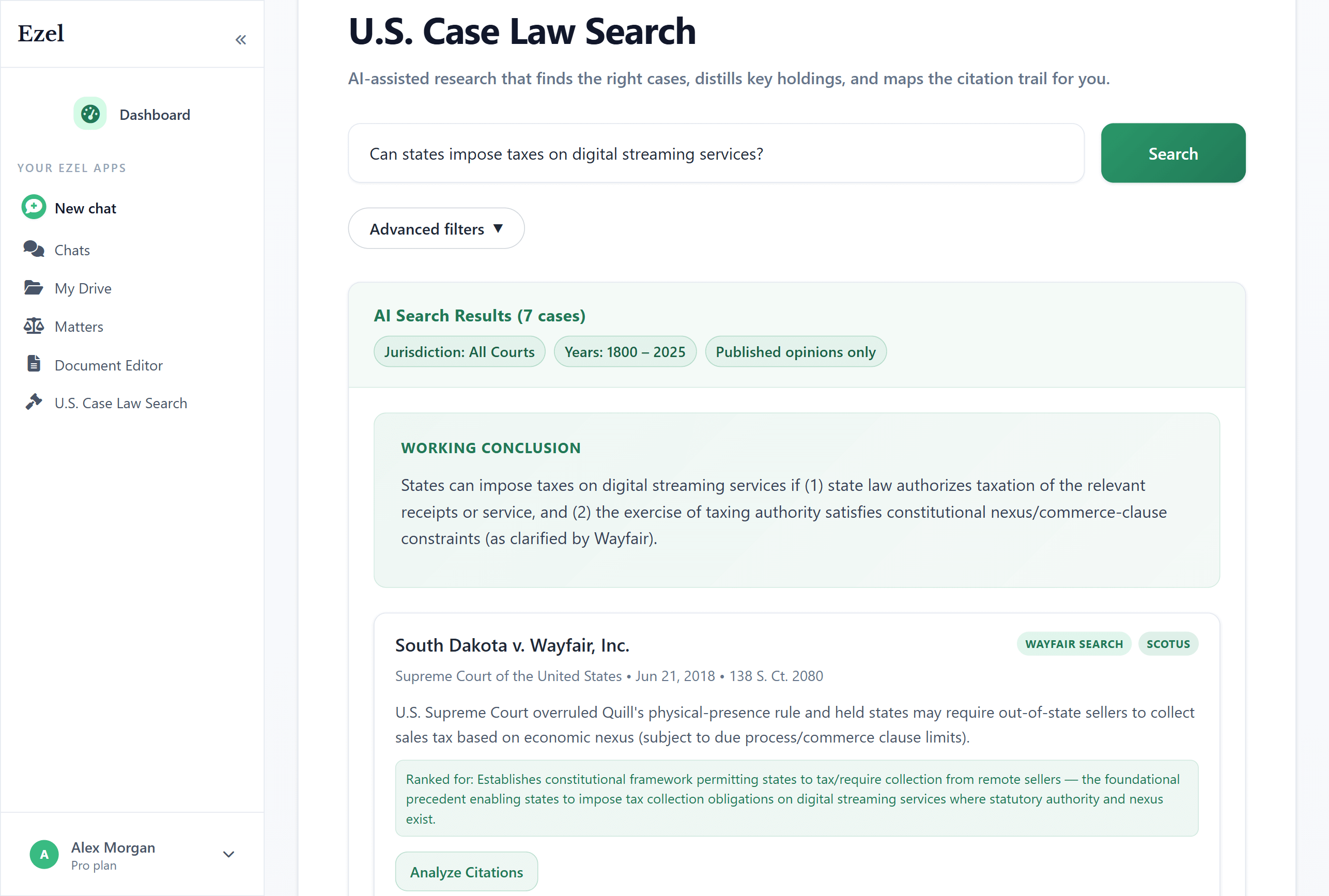

Search like you think

Describe your legal question in plain English. Filter by jurisdiction, date, and court level. Read full opinions without leaving Ezel.

- All 50 states plus federal courts

- Natural language queries - no boolean syntax

- Citation analysis and network exploration

- Copy quotes with automatic citation generation

Ready to transform your legal workflow?

Join legal teams using Ezel to draft documents, research case law, and organize matters — all in one workspace.