FORMAL RESPONSE TO IRS NOTICE OF EXAMINATION

(“Tax Audit Response”)

[// GUIDANCE: This template is designed for use by attorneys representing individual or business taxpayers in connection with a federal income tax examination. Modify bracketed placeholders and optional provisions to fit the specific facts, examination posture, and client objectives.]

TABLE OF CONTENTS

- Document Header

- Definitions

- Operative Provisions

- Representations & Warranties

- Covenants & Restrictions

- Default & Remedies

- Risk Allocation

- Dispute Resolution

- General Provisions

- Execution Block

1. DOCUMENT HEADER

1.1 Title.

FORMAL RESPONSE TO IRS NOTICE OF EXAMINATION DATED [DATE]

1.2 Parties.

This Tax Audit Response (the “Response”) is submitted by [Taxpayer Legal Name], a [state] [entity type/individual] with taxpayer identification number [TIN] (“Taxpayer”), through its duly authorized representative [Representative Name and Firm, if any] (collectively with Taxpayer, “Respondent”), to the Internal Revenue Service, Examination Division, [Campus/Office] (“IRS”).

1.3 Effective Date.

This Response is effective as of [Effective Date] (the “Effective Date”).

1.4 Recitals.

A. On [Notice Date], IRS issued to Taxpayer a [30-Day Letter / Form 4564 / Letter 2205 / other] (the “Audit Notice”) initiating an examination of Taxpayer’s federal income tax return for the taxable period ending [Tax Year/Period] (the “Examination Period”).

B. In accordance with 26 U.S.C. §§ 6201, 7602, and 6213, Taxpayer is afforded the opportunity to present information, explanations, and supporting documentation before any final deficiency determination.

C. Taxpayer, by and through this Response, respectfully submits its position, documentation, and legal authorities, and requests resolution consistent with applicable federal tax law.

2. DEFINITIONS

For purposes of this Response, capitalized terms have the meanings set forth below. Terms defined in the singular include the plural and vice-versa.

“Administrative File” means the complete set of documents, correspondence, workpapers, and electronic records maintained by IRS relating to the Examination.

“Audit Notice” has the meaning set forth in Recital A.

“Disputed Item(s)” means each proposed adjustment, disallowance, or penalty described in the Exam Report or Audit Notice.

“Examination” means the federal income tax examination of Taxpayer’s return for the Examination Period.

“Examination Period” has the meaning set forth in Recital A.

“IRS” has the meaning set forth in Section 1.2.

“Representative” means any attorney, certified public accountant, or enrolled agent duly authorized under a valid Form 2848 Power of Attorney on file with IRS for this Examination.

“Response” means this formal submission, together with all Attachments, Schedules, Exhibits, and Supporting Documentation.

“Supporting Documentation” means all books, records, computations, affidavits, and other materials provided with or referenced in this Response.

3. OPERATIVE PROVISIONS

3.1 Statement of Compliance.

Taxpayer hereby responds to the Audit Notice in good faith and in compliance with 26 U.S.C. § 7602 and all applicable Treasury Regulations.

3.2 Response to Disputed Items.

A. Schedule 1 (attached) sets forth each Disputed Item, IRS’s proposed adjustment, Taxpayer’s legal and factual position, and citations to Supporting Documentation.

B. For each Disputed Item, Taxpayer provides contemporaneous records, reconciliations, and explanatory narratives sufficient to carry the burden of production under 26 U.S.C. § 7491(a), to the extent applicable.

3.3 Production of Records.

Simultaneously with this Response, Taxpayer produces the Supporting Documentation itemized in Schedule 2. Any additional documents requested pursuant to a valid Information Document Request (“IDR”) will be furnished within [number] calendar days after receipt of such IDR, or as otherwise mutually agreed in writing.

3.4 Conference Request.

Pursuant to IRS administrative procedures, Taxpayer requests an in-person or virtual conference with the assigned Revenue Agent and/or Immediate Supervisor within [number] days of IRS’s receipt of this Response to discuss resolution of the Disputed Items.

3.5 Conditions Precedent.

Taxpayer’s obligations hereunder are conditioned upon (i) acknowledgment of receipt of this Response by IRS, and (ii) timely scheduling of the conference requested in Section 3.4.

4. REPRESENTATIONS & WARRANTIES

4.1 Authority.

Taxpayer represents that the individual executing this Response is duly authorized and empowered to act on Taxpayer’s behalf.

4.2 Accuracy and Completeness.

Taxpayer warrants, to the best of its knowledge after reasonable inquiry, that all factual statements and Supporting Documentation provided herein are true, correct, and complete in all material respects as of the Effective Date.

4.3 Survival.

The representations and warranties in this Section 4 survive the conclusion of the Examination and any subsequent administrative or judicial proceedings.

5. COVENANTS & RESTRICTIONS

5.1 Continuing Cooperation.

Taxpayer covenants to (i) maintain and preserve all records relevant to the Examination until the expiration of all applicable statutes of limitation, (ii) supplement this Response promptly upon discovery of any material inaccuracy, and (iii) comply with all lawful and properly issued IDRs.

5.2 Notice of Changes.

Taxpayer shall notify IRS in writing within [number] days of any material change to the facts, documentation, or legal authority relied upon in this Response.

5.3 No Waiver of Rights.

Nothing in this Response shall be construed as a waiver of Taxpayer’s rights to Collection Due Process, Appeals Office review, refund claims, Tax Court petition, or any other remedies available under federal tax law.

6. DEFAULT & REMEDIES

6.1 Events of Default.

The following constitute events of default (“Default”):

a. Failure by Taxpayer to timely respond to a valid IDR after reasonable extensions.

b. Material misstatement or omission in this Response.

6.2 Cure Period.

Upon written notice of Default from IRS, Taxpayer shall have [30] calendar days to cure the Default to IRS’s reasonable satisfaction.

6.3 Remedies.

If a Default is not timely cured, IRS may proceed with issuance of a Notice of Proposed Adjustment, Statutory Notice of Deficiency, or other enforcement action permitted by law, subject to Taxpayer’s administrative and judicial appeal rights.

6.4 Attorneys’ Fees and Costs.

Each party shall bear its own attorneys’ fees and costs, except as otherwise provided under 26 U.S.C. § 7430 or other applicable law.

7. RISK ALLOCATION

7.1 Burden of Proof.

Taxpayer acknowledges that, except as otherwise provided in 26 U.S.C. § 7491, the burden of proof rests with Taxpayer to substantiate its tax positions.

7.2 Additional Tax, Penalties, and Interest.

Taxpayer recognizes that, should IRS prevail with respect to any Disputed Item, Taxpayer may be liable for additional tax, statutory interest under 26 U.S.C. § 6601, and applicable penalties (e.g., accuracy-related penalties under 26 U.S.C. § 6662).

7.3 Indemnification of Representative.

Taxpayer agrees to indemnify and hold harmless its Representative from and against any third-party claims arising from Representative’s reliance on information supplied by Taxpayer, except to the extent finally determined to have resulted from Representative’s gross negligence or willful misconduct.

[// GUIDANCE: Modify or omit Section 7.3 if no third-party representative is involved.]

8. DISPUTE RESOLUTION

8.1 Governing Law.

This Response and all disputes arising out of or related hereto are governed exclusively by the Internal Revenue Code and other applicable federal tax law.

8.2 Forum Selection.

Any administrative dispute shall proceed before IRS Examination Division, Appeals Office, or other authorized administrative forum. Judicial review, if necessary, shall be sought in the United States Tax Court, U.S. District Court, or U.S. Court of Federal Claims, as appropriate under 26 U.S.C. §§ 6213, 7422, and related provisions.

8.3 Arbitration.

Arbitration is not available for federal tax controversies except as specifically authorized under IRS administrative programs, which are not invoked herein.

8.4 Jury Waiver.

Because disputes are resolved in administrative or Article I courts where jury trials are unavailable, the parties acknowledge that jury trial rights are inapplicable.

9. GENERAL PROVISIONS

9.1 Amendments and Waivers.

Any amendment or waiver of this Response must be in writing and signed by Taxpayer (or Representative) and acknowledged by IRS.

9.2 Assignment.

Taxpayer may not assign rights or delegate duties under this Response without prior written consent of IRS, except that Taxpayer may substitute counsel or Representative by filing a new Form 2848.

9.3 Successors and Assigns.

This Response is binding upon Taxpayer and its successors and assigns and inures to the benefit of IRS and its authorized agents.

9.4 Severability.

If any provision of this Response is held invalid, the remaining provisions shall remain in full force to the maximum extent permitted by law.

9.5 Integration.

This Response, including all Schedules and Attachments, constitutes the entire submission of Taxpayer concerning the Audit Notice and supersedes all prior oral or written communications on the subject matter hereof.

9.6 Counterparts; Electronic Signatures.

This Response may be executed in counterparts, each of which is deemed an original, and all of which constitute one instrument. Signatures transmitted by facsimile, PDF, or compliant e-signature platform are deemed original for all purposes.

10. EXECUTION BLOCK

IN WITNESS WHEREOF, the undersigned executes and submits this Response as of the Effective Date.

| Taxpayer | Representative (if applicable) |

|---|---|

| [TAXPAYER LEGAL NAME] | [REPRESENTATIVE NAME], [CREDENTIAL] |

| By: ___________________________ | By: ___________________________ |

| Name: [Signer Name] | Name: [Rep. Signer Name] |

| Title: [Title, if entity] | Title: [Attorney / CPA / EA] |

| Date: _________________________ | Date: _________________________ |

[Optional Notary Block – include if required under state law for verifications.]

SCHEDULE 1 – DETAILED RESPONSE TO DISPUTED ITEMS

[Insert table with columns: Line/Issue, IRS Proposed Adjustment, Taxpayer Position, Legal Authority, Supporting Documentation Reference.]

SCHEDULE 2 – INDEX OF SUPPORTING DOCUMENTATION

[Insert descriptive list of attached documents, organized by Bates number or exhibit label.]

[// GUIDANCE: Before filing, confirm that all factual statements are verified, citations are accurate, Schedules are complete, and Form 2848 (or other authorization) is current. Tailor cure periods, timelines, and indemnification language to client strategy and applicable IRS guidance.]

Do more with Ezel

This free template is just the beginning. See how Ezel helps legal teams draft, research, and collaborate faster.

AI that drafts while you watch

Tell the AI what you need and watch your document transform in real-time. No more copy-pasting between tools or manually formatting changes.

- Natural language commands: "Add a force majeure clause"

- Context-aware suggestions based on document type

- Real-time streaming shows edits as they happen

- Milestone tracking and version comparison

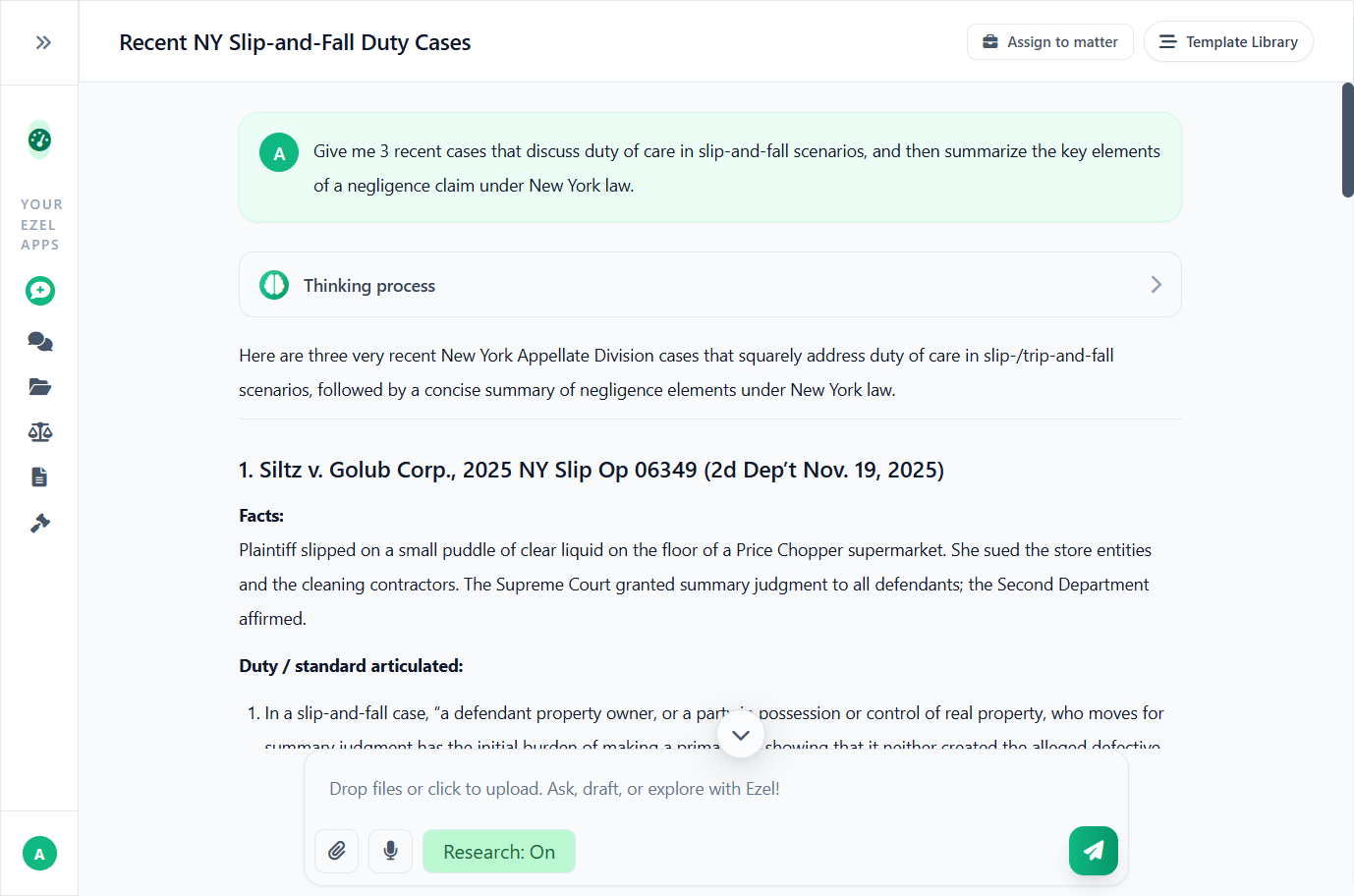

Research and draft in one conversation

Ask questions, attach documents, and get answers grounded in case law. Link chats to matters so the AI remembers your context.

- Pull statutes, case law, and secondary sources

- Attach and analyze contracts mid-conversation

- Link chats to matters for automatic context

- Your data never trains AI models

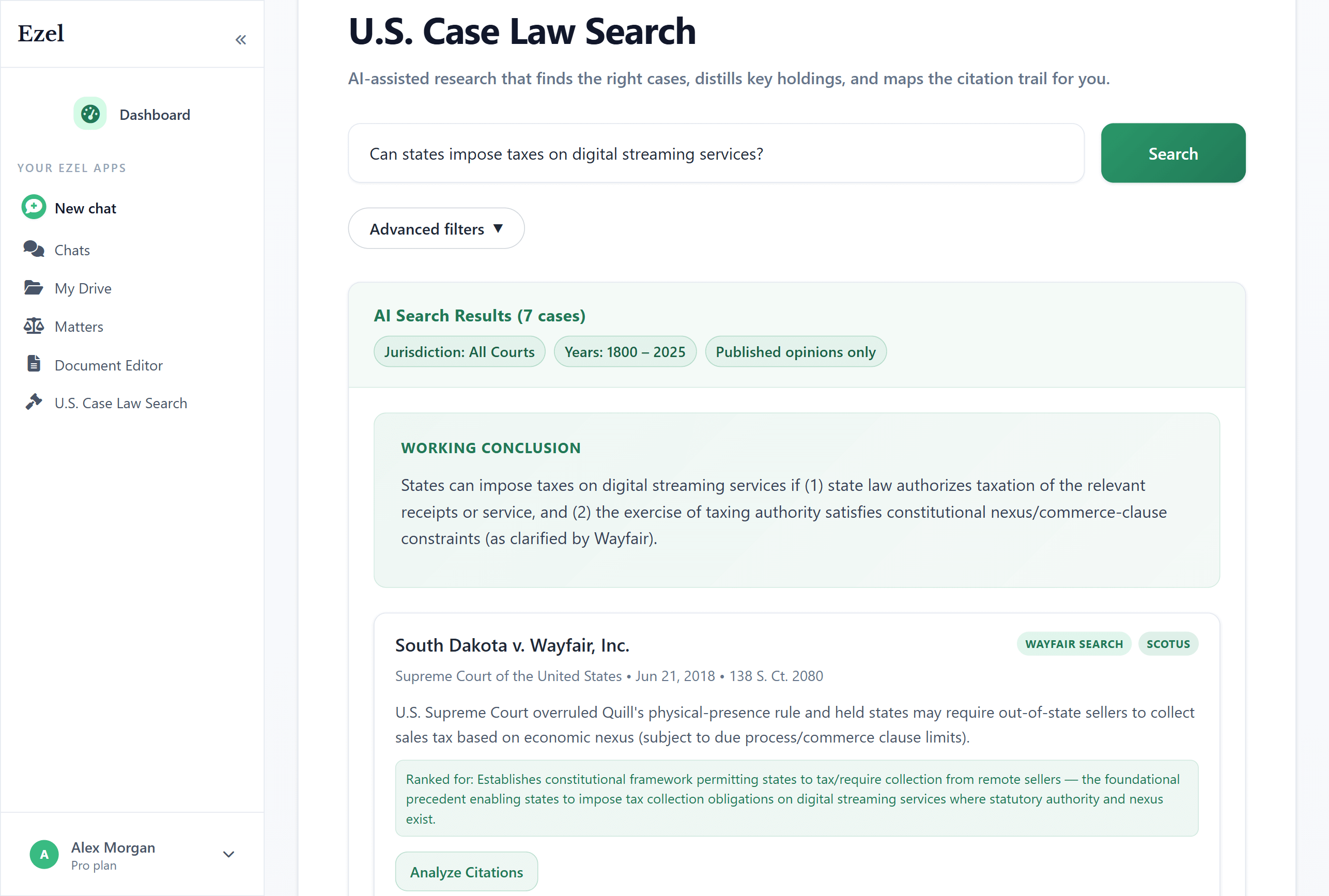

Search like you think

Describe your legal question in plain English. Filter by jurisdiction, date, and court level. Read full opinions without leaving Ezel.

- All 50 states plus federal courts

- Natural language queries - no boolean syntax

- Citation analysis and network exploration

- Copy quotes with automatic citation generation

Ready to transform your legal workflow?

Join legal teams using Ezel to draft documents, research case law, and organize matters — all in one workspace.